Loan default risk prediction

The project comes from the Kaggle competition. It is required to predict whether the customer's loan will default according to the customer's credit card information, installment information, credit bureau information and so on.

Load module and build environment

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

plt.rcParams['font.sans-serif'] = ['SimHei']

import seaborn as sns

import warnings

# Ignore warning

warnings.filterwarnings("ignore")

# IPython magic function, embedded drawing, PLT can be omitted Show() to display the image directly

%matplotlib inline

CSV data reading

train=pd.read_csv(r"C:\Users\TP\Desktop\myself\Loan risk\Credit risk data set\application_train.csv") test=pd.read_csv(r"C:\Users\TP\Desktop\myself\Loan risk\Credit risk data set\application_test.csv") train.sample(10)

| SK_ID_CURR | TARGET | NAME_CONTRACT_TYPE | CODE_GENDER | FLAG_OWN_CAR | FLAG_OWN_REALTY | CNT_CHILDREN | AMT_INCOME_TOTAL | AMT_CREDIT | AMT_ANNUITY | ... | FLAG_DOCUMENT_18 | FLAG_DOCUMENT_19 | FLAG_DOCUMENT_20 | FLAG_DOCUMENT_21 | AMT_REQ_CREDIT_BUREAU_HOUR | AMT_REQ_CREDIT_BUREAU_DAY | AMT_REQ_CREDIT_BUREAU_WEEK | AMT_REQ_CREDIT_BUREAU_MON | AMT_REQ_CREDIT_BUREAU_QRT | AMT_REQ_CREDIT_BUREAU_YEAR | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 74327 | 186199 | 0 | Cash loans | M | N | Y | 0 | 157500.0 | 640080.0 | 24259.5 | ... | 0 | 0 | 0 | 0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 |

| 105101 | 221958 | 0 | Cash loans | F | N | Y | 0 | 247500.0 | 1288350.0 | 37795.5 | ... | 0 | 0 | 0 | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 3.0 |

| 89301 | 203680 | 0 | Revolving loans | M | Y | Y | 0 | 225000.0 | 225000.0 | 11250.0 | ... | 0 | 0 | 0 | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 185992 | 315612 | 1 | Cash loans | F | Y | Y | 1 | 225000.0 | 562500.0 | 30645.0 | ... | 0 | 0 | 0 | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 2.0 |

| 254717 | 394747 | 0 | Cash loans | F | N | Y | 0 | 202500.0 | 405000.0 | 24601.5 | ... | 0 | 0 | 0 | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 2.0 |

| 57672 | 166832 | 0 | Cash loans | M | N | N | 2 | 157500.0 | 427450.5 | 23319.0 | ... | 0 | 0 | 0 | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 2.0 | 4.0 |

| 196040 | 327318 | 0 | Cash loans | M | Y | N | 0 | 112500.0 | 276277.5 | 14233.5 | ... | 0 | 0 | 0 | 0 | NaN | NaN | NaN | NaN | NaN | NaN |

| 70982 | 182323 | 0 | Cash loans | F | N | Y | 1 | 117000.0 | 271066.5 | 13968.0 | ... | 0 | 0 | 0 | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 |

| 156304 | 281183 | 0 | Revolving loans | F | N | N | 1 | 90000.0 | 270000.0 | 13500.0 | ... | 0 | 0 | 0 | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 |

| 149247 | 273036 | 0 | Cash loans | M | N | Y | 2 | 144000.0 | 562500.0 | 26064.0 | ... | 1 | 0 | 0 | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 |

10 rows × 122 columns

Data cleaning

Missing value and abnormal value handling

Missing value

# Missing value detection, function definition

def mis_val(data):

mis_val=data.isnull().sum().reset_index().rename(columns={"index":"feature",0:"mis_tol"})

l=len(mis_val)

mis_val["mis_per"]=(mis_val.mis_tol/len(data)*100).round(1)

mis_nol=len(mis_val[mis_val.mis_tol==0])

mis_num=len(mis_val[mis_val.mis_tol != 0])

mis=mis_val[mis_val.mis_tol != 0].sort_values("mis_tol",ascending=False,ignore_index=True)

print("Total yes"+str(l)+"column,\n"

"among"+str(mis_nol)+"Column has no missing value,\n"

"surplus"+str(mis_num)+"Column has missing values.")

return mis

mis_val(train)

There are 122 columns in total, There are no missing values in 55 columns, The remaining 67 columns have missing values.

| feature | mis_tol | mis_per | |

|---|---|---|---|

| 0 | COMMONAREA_MEDI | 214865 | 69.9 |

| 1 | COMMONAREA_AVG | 214865 | 69.9 |

| 2 | COMMONAREA_MODE | 214865 | 69.9 |

| 3 | NONLIVINGAPARTMENTS_MEDI | 213514 | 69.4 |

| 4 | NONLIVINGAPARTMENTS_MODE | 213514 | 69.4 |

| ... | ... | ... | ... |

| 62 | EXT_SOURCE_2 | 660 | 0.2 |

| 63 | AMT_GOODS_PRICE | 278 | 0.1 |

| 64 | AMT_ANNUITY | 12 | 0.0 |

| 65 | CNT_FAM_MEMBERS | 2 | 0.0 |

| 66 | DAYS_LAST_PHONE_CHANGE | 1 | 0.0 |

67 rows × 3 columns

Since the LGB model we use later is not sensitive to missing values, in order to simplify the process, the missing values will not be interpreted here. For some cases with the same missing rate of columns, further analysis is needed, and further processing will be carried out in the feature engineering part. If other models sensitive to missing values are used, the columns with missing values need to be processed one by one. The common processing methods of missing values include: delete and fill;

Outliers

Outliers: sometimes the dataset contains one or more values with abnormally large or small values. Such extreme values are called outliers

There are many ways to judge and deal with outliers, such as 3 Sigma method, percentile method, MAD method and so on

Here, we take the simplest method to describe statistics, that is, to view the mean, maximum, minimum and other information of the characteristics, and judge whether there are abnormal values in combination with the actual business

View the data distribution of user age

(train["DAYS_BIRTH"]/-365).describe()

count 307511.000000 mean 43.936973 std 11.956133 min 20.517808 25% 34.008219 50% 43.150685 75% 53.923288 max 69.120548 Name: DAYS_BIRTH, dtype: float64

It is found that the distribution of data is relatively normal. The maximum age is 69 years old and the minimum age is 20 years old. There are no very abnormal figures

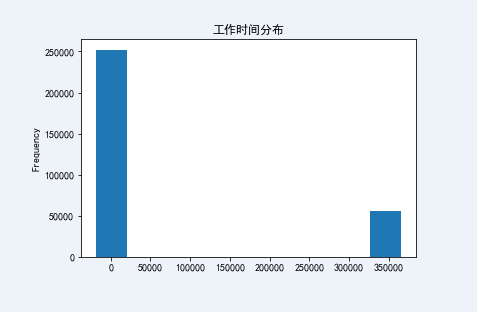

View the working time distribution of users and find

(train['DAYS_EMPLOYED']/-365).describe()

count 307511.000000 mean -174.835742 std 387.056895 min -1000.665753 25% 0.791781 50% 3.323288 75% 7.561644 max 49.073973 Name: DAYS_EMPLOYED, dtype: float64

The minimum value is - 1000 years, which is obviously an abnormal data. No one's working hours are negative, which is an abnormal value

# View working hours days_ Employee data distribution train['DAYS_EMPLOYED'].plot.hist(title = 'Working time distribution')

<matplotlib.axes._subplots.AxesSubplot at 0x2b1a78e0>

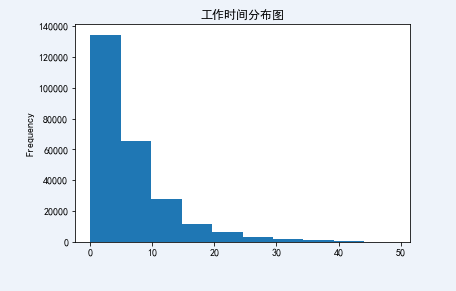

Here, null values are used to replace outliers (whether 0 value, average value, median, etc. will change the data distribution, and LGB model allows the data to be null)

train['DAYS_EMPLOYED'].replace({365243: np.nan}, inplace = True)

(train['DAYS_EMPLOYED']/-365).plot.hist(title = 'Working time distribution')

<matplotlib.axes._subplots.AxesSubplot at 0x2be6ff70>

The outliers are erased. After replacement, let's take a look at the distribution of working hours. It's much normal

View the gender distribution of users and find

train.groupby("CODE_GENDER").size()

CODE_GENDER F 202448 M 105059 XNA 4 dtype: int64

It is found that there is an abnormal value "XNA" in the user's gender. Since there are only four abnormal values, whether they are replaced by null values, F and m, they will not affect the result model and prediction results, so fill in M for the time being

train.CODE_GENDER.replace("XNA","M",inplace=True)

train.groupby("CODE_GENDER").size()

CODE_GENDER F 202448 M 105063 dtype: int64

Check the service life distribution of the customer's car and find

train.OWN_CAR_AGE.describe()

count 104582.000000 mean 12.061091 std 11.944812 min 0.000000 25% 5.000000 50% 9.000000 75% 15.000000 max 91.000000 Name: OWN_CAR_AGE, dtype: float64

sns.set_style("darkgrid")

sns.boxplot(x=train.OWN_CAR_AGE,orient="v",width=0.3)

<matplotlib.axes._subplots.AxesSubplot at 0x290830d0>

If we judge the abnormal value according to the upper limit of the box diagram, the service life of the customer's car greater than 30 is the abnormal value. The actual business needs to be combined with the actual situation. The outlier limit is not necessarily 30. In this exercise, we tentatively set the upper limit of the box chart as the outlier limit;

# We fill the outliers with the upper boundary, which is 30 train.OWN_CAR_AGE[train.OWN_CAR_AGE>30]=30 # Note that if it is written as train [train. Own_car_age > 30] OWN_ CAR_ Age = 30 does not replace any data, and the reason is unknown

In actual business, abnormal value detection and processing should be carried out for each feature, and existing abnormal value processing functions / modules should be defined or adopted. Here, the process is simplified and will not be handled one by one;

Exploration of default user portrait

The goal of this part of analysis is to check the characteristic distribution of defaulting users and non defaulting users. The goal is to establish a basic understanding of the portrait of defaulting users and lay a foundation for subsequent feature engineering. For example, there are many fields in the data set, including gender, age, working hours, etc. are men more likely to default or women? Are older people more likely to default or younger people? Viewing these data can help us have a better understanding of the data. At the same time, if a field is not sensitive to the characteristic distribution of whether the user defaults, we can consider whether to delete this field.

Chart function definition

Define discrete chart functions

def discrete_bar(data,label,n=10):

# Calculate label default rate

group_label_0=data.groupby(label).TARGET.agg(["sum","count"])

group_label_1=group_label_0.reset_index()

group_label_1.columns=[label,"TARGET_SUM","TARGET_COUNT"]

group_label_1["Default_Rate"]=(group_label_1["TARGET_SUM"]/group_label_1["TARGET_COUNT"]*100).round(2)

group_label_1.sort_values(by="Default_Rate",ascending=False,inplace=True,ignore_index=True)

print(group_label_1)

# The chart shows that the histogram is used when the discrete value is small

if len(group_label_1)<n:

plt.figure(figsize=(14,8))

sns.set_style("darkgrid")

# label quantity distribution of each category

plt.subplot(1,2,1)

ax0=sns.barplot(x=label,y="TARGET_COUNT",data=group_label_1)

ax0.set_xticklabels(group_label_1[label],rotation=45)

x0=group_label_1[label]

y0=group_label_1["TARGET_COUNT"]

for i ,j in zip(np.arange(len(x0)),y0):

plt.text(i,j+np.mean(y0)/50,j,horizontalalignment="center")

# Distribution chart of default rate of label

plt.subplot(1,2,2)

ax1=sns.barplot(x=label,y="Default_Rate",data=group_label_1)

ax1.set_xticklabels(group_label_1[label],rotation=45)

x1=group_label_1[label]

y1=group_label_1["Default_Rate"]

for i ,j in zip(np.arange(len(x1)),y1):

plt.text(i,j+0.2,j,horizontalalignment="center")

# The chart shows that the bar chart is used when there are many discrete values

else:

plt.figure(figsize=(16,10))

sns.set_style("whitegrid")

# label quantity distribution of each category

plt.subplot(1,2,1)

ax0=sns.barplot(x="TARGET_COUNT",y=label,data=group_label_1,orient="h")

ax0.set_yticklabels(group_label_1[label],rotation=75)

x0=group_label_1[label]

y0=group_label_1["TARGET_COUNT"]

for i ,j in zip(np.arange(len(x0)),y0):

plt.text(j+np.mean(y0)/5,i,j,horizontalalignment="center")

# Distribution chart of default rate of label

plt.subplot(1,2,2)

ax1=sns.barplot(x="Default_Rate",y=label,data=group_label_1,orient="h")

ax1.set_yticklabels(group_label_1[label],rotation=75)

x1=group_label_1[label]

y1=group_label_1["Default_Rate"]

for i ,j in zip(np.arange(len(x1)),y1):

plt.text(j+1,i,j,horizontalalignment="center")

Define continuous chart functions

def continuous_plot(data,label,cutn=8):

plt.figure(figsize=(12,12))

# Draw the nuclear density curve of default users and normal users

plt.subplot(2,1,1)

sns.set_style("darkgrid")

sns.kdeplot(data[label][data["TARGET"]==0])

sns.kdeplot(data[label][data["TARGET"]==1])

# Segment the fields to calculate the default rate

lb=data[[label,"TARGET"]]

nln=label+"_CUT"

lb[nln]=pd.cut(lb[label],cutn)

lb_group=lb.groupby(nln)["TARGET"].agg(["sum","count"])

lb_group["pro"]=(lb_group["sum"]/lb_group["count"]*100).round(2)

lb_group.reset_index(inplace=True)

print("Default rate of each segment\n\n",lb_group)

plt.subplot(2,1,2)

ax=sns.barplot(x=nln,y="pro",data=lb_group)

ax.set_xticklabels(lb_group[nln],rotation=45)

Unified chart function

def chart_fuc(data,label,con_ornot="dispersed",n=10,cutn=8):

if con_ornot=="dispersed":

discrete_bar(data,label,n)

elif con_ornot=="continuity" :

continuous_plot(data,label,cutn)

Feature distribution image of each field

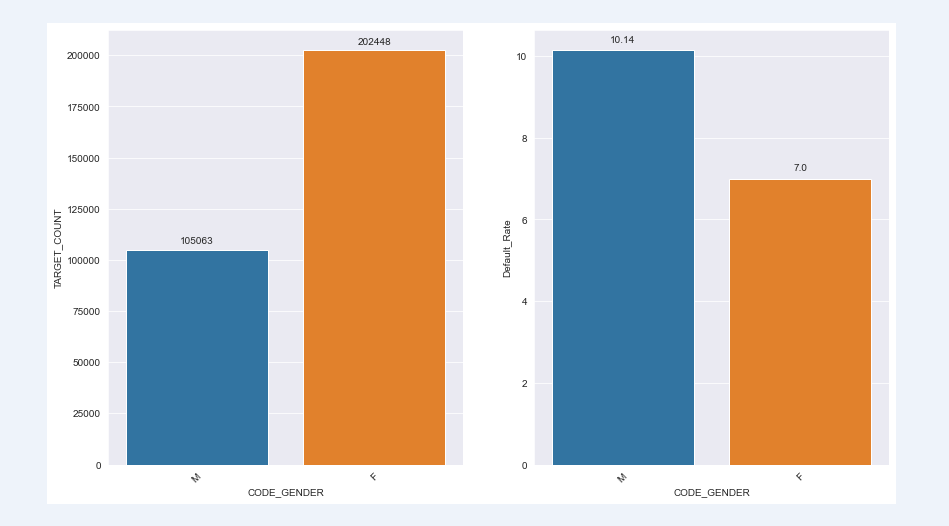

First, let's take a look at the default rate of male and female users. It is found that the default rate of male users is higher, with 10.14% for male users and 7% for women

chart_fuc(train,"CODE_GENDER")

CODE_GENDER TARGET_SUM TARGET_COUNT Default_Rate 0 M 10655 105063 10.14 1 F 14170 202448 7.00

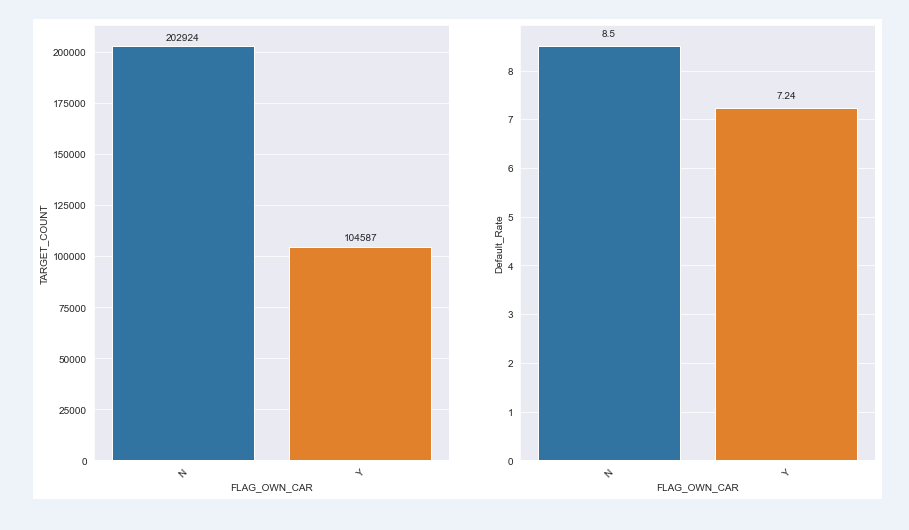

The default rate of users with cars is lower than that of users without cars. The default rate of users with cars is 7.24% and that of users without cars is 8.5%;

chart_fuc(train,"FLAG_OWN_CAR")

FLAG_OWN_CAR TARGET_SUM TARGET_COUNT Default_Rate 0 N 17249 202924 8.50 1 Y 7576 104587 7.24

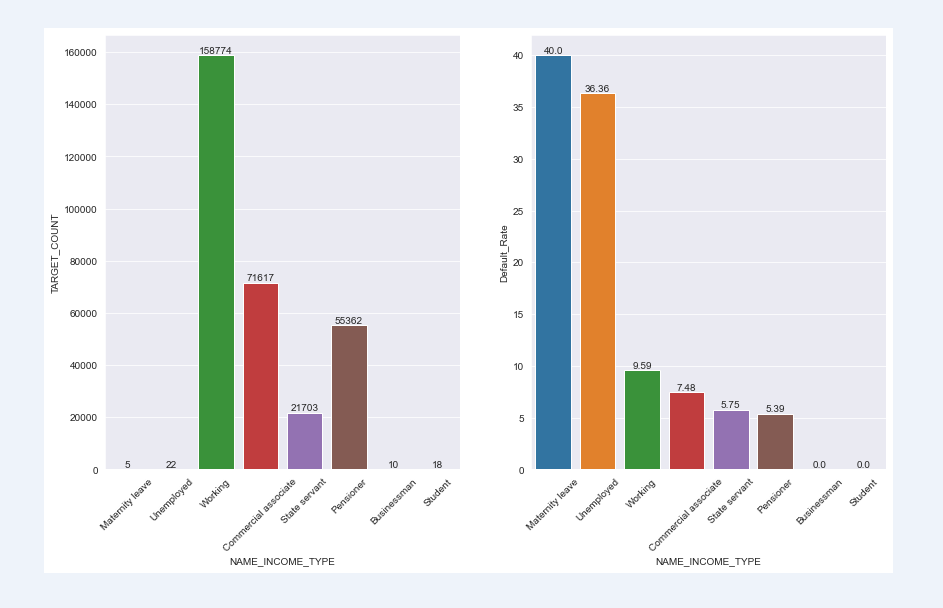

The default rate varies significantly with different types of user income; The default rate of employees taking maternity leave and unemployed is significantly higher than that of other income groups, among which the default rate of businessmen and students is 0;

chart_fuc(train,"NAME_INCOME_TYPE")

NAME_INCOME_TYPE TARGET_SUM TARGET_COUNT Default_Rate 0 Maternity leave 2 5 40.00 1 Unemployed 8 22 36.36 2 Working 15224 158774 9.59 3 Commercial associate 5360 71617 7.48 4 State servant 1249 21703 5.75 5 Pensioner 2982 55362 5.39 6 Businessman 0 10 0.00 7 Student 0 18 0.00

Users have different occupational types and different default rates, among which the default rate of low skilled workers is the highest, as high as 17.15%; The professional default rate of Accountants is the lowest, only 4.83%

chart_fuc(train,"OCCUPATION_TYPE")

OCCUPATION_TYPE TARGET_SUM TARGET_COUNT Default_Rate 0 Low-skill Laborers 359 2093 17.15 1 Drivers 2107 18603 11.33 2 Waiters/barmen staff 152 1348 11.28 3 Security staff 722 6721 10.74 4 Laborers 5838 55186 10.58 5 Cooking staff 621 5946 10.44 6 Sales staff 3092 32102 9.63 7 Cleaning staff 447 4653 9.61 8 Realty agents 59 751 7.86 9 Secretaries 92 1305 7.05 10 Medicine staff 572 8537 6.70 11 Private service staff 175 2652 6.60 12 IT staff 34 526 6.46 13 HR staff 36 563 6.39 14 Core staff 1738 27570 6.30 15 Managers 1328 21371 6.21 16 High skill tech staff 701 11380 6.16 17 Accountants 474 9813 4.83

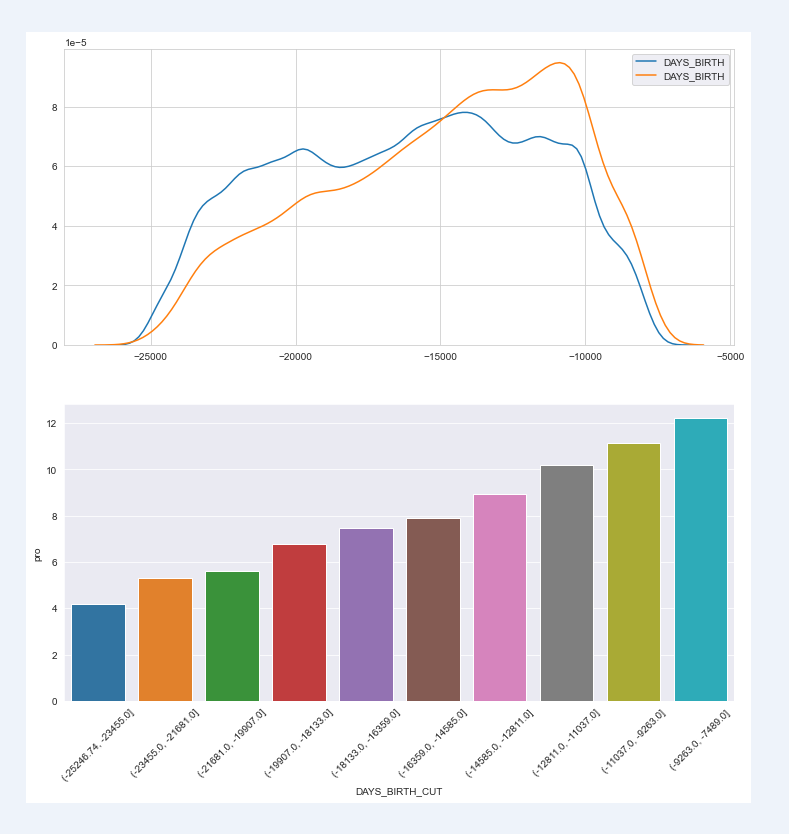

User age distribution: because age is a continuous variable, use and distribution diagram to view user distribution (histogram can also well describe the distribution); Then through the histogram to show the default rate, we can clearly see that the younger the age, the higher the default rate;

chart_fuc(train,"DAYS_BIRTH",con_ornot="continuity",cutn=10)

Default rate of each segment

DAYS_BIRTH_CUT sum count pro

0 (-25246.74, -23455.0] 503 11977 4.20

1 (-23455.0, -21681.0] 1466 27685 5.30

2 (-21681.0, -19907.0] 1826 32650 5.59

3 (-19907.0, -18133.0] 2278 33544 6.79

4 (-18133.0, -16359.0] 2558 34339 7.45

5 (-16359.0, -14585.0] 3185 40356 7.89

6 (-14585.0, -12811.0] 3737 41746 8.95

7 (-12811.0, -11037.0] 3916 38424 10.19

8 (-11037.0, -9263.0] 3687 33111 11.14

9 (-9263.0, -7489.0] 1669 13679 12.20

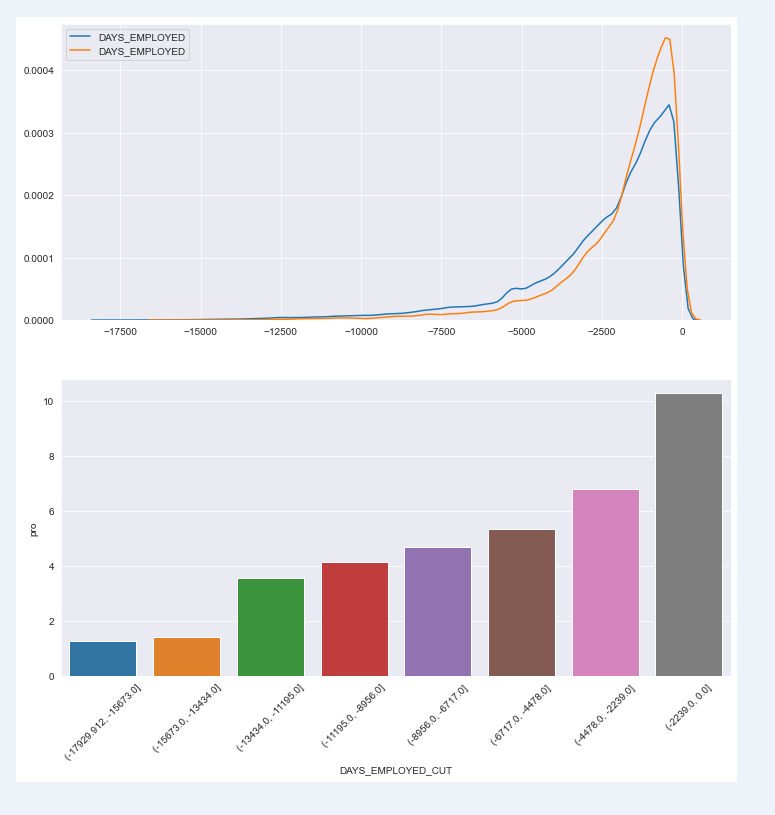

The default distribution of users' employment days is extremely obvious. The fewer employment days, the higher the default rate of users

chart_fuc(train,"DAYS_EMPLOYED",con_ornot="continuity")

Default rate of each segment

DAYS_EMPLOYED_CUT sum count pro

0 (-17929.912, -15673.0] 1 79 1.27

1 (-15673.0, -13434.0] 8 570 1.40

2 (-13434.0, -11195.0] 72 2028 3.55

3 (-11195.0, -8956.0] 166 4007 4.14

4 (-8956.0, -6717.0] 413 8828 4.68

5 (-6717.0, -4478.0] 1104 20719 5.33

6 (-4478.0, -2239.0] 4181 61310 6.82

7 (-2239.0, 0.0] 15890 154596 10.28

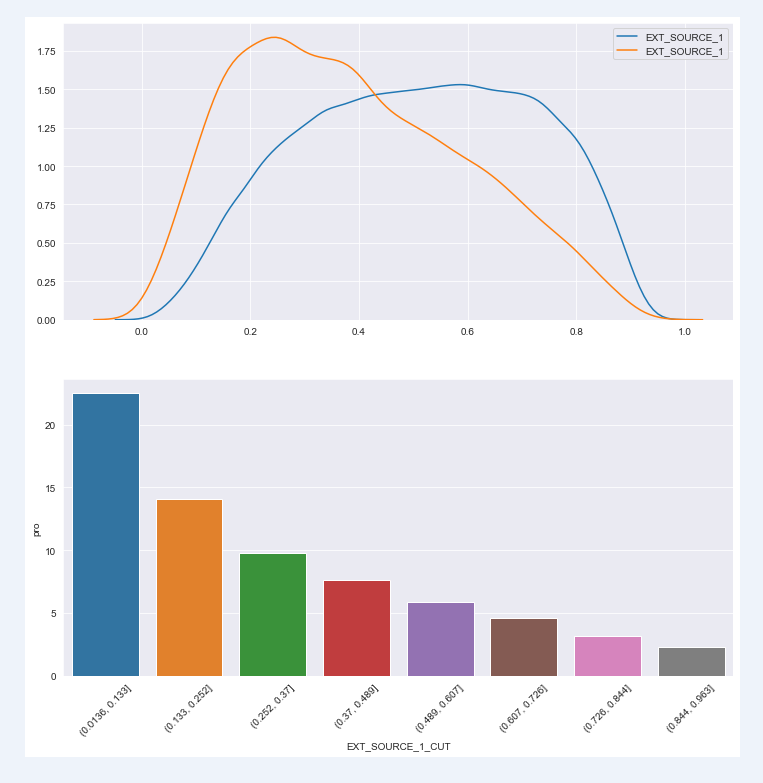

There is a corresponding relationship between external data source standardization score and default rate. The lower the external data source standardization score, the higher the default rate;

chart_fuc(train,"EXT_SOURCE_1",con_ornot="continuity")

Default rate of each segment EXT_SOURCE_1_CUT sum count pro 0 (0.0136, 0.133] 978 4344 22.51 1 (0.133, 0.252] 2112 15024 14.06 2 (0.252, 0.37] 2057 21026 9.78 3 (0.37, 0.489] 1778 23240 7.65 4 (0.489, 0.607] 1380 23670 5.83 5 (0.607, 0.726] 1045 22891 4.57 6 (0.726, 0.844] 581 18587 3.13 7 (0.844, 0.963] 123 5351 2.30

In addition, the user's marriage, whether there are children, the number of family members, living area and other factors have an impact on the default rate. You can call chart one by one_ Fuc function to view user distribution map and user default rate distribution map

Characteristic Engineering

"Data and features determine the upper limit of machine learning, while models and algorithms only approach this upper limit". Feature engineering refers to the process of transforming the original data into the training data of the model. Its purpose is to obtain better training data features and make the machine learning model approach this upper limit. Generally speaking, it includes three parts: feature construction, feature extraction and feature selection;

Feature construction refers to manually finding some physical features from the original data.

Feature extraction: principal component analysis, LDA linear discriminant analysis, independent component analysis

Feature selection is to eliminate irrelevant or redundant features, reduce the number of effective features, reduce the time of model training and improve the accuracy of the model.

For Feature Engineering, see: https://www.cnblogs.com/wxquare/p/5484636.html

Combined with business understanding, build features

-

CREDIT_INCOME_PERCENT: loan amount / customer income, AMT_CREDIT/AMT_INCOME_TOTAL, it is expected that the greater the ratio, the greater the possibility of user default

-

ANNUITY_INCOME_PERCENT: annual repayment amount of loan / customer income, AMT_ ANNUITY/AMT_ INCOME_ The total logic is consistent with the above

-

CREDIT_TERM: annual repayment amount of loan / loan amount, repayment cycle of loan, AMT_ANNUITY /AMT_CREDIT, the repayment cycle is a common way of risk management of credit institutions. Theoretically, the customer risk is large, and the credit institutions will shorten the repayment cycle. The distribution map of repayment cycle and default rate should show some information;

-

DAYS_EMPLOYED_PERCENT: user working time / user age, DAYS_EMPLOYED/DAYS_BIRTH

-

INCOME_PER_CHILD: customer income / number of children, AMT_INCOME_TOTAL /CNT_CHILDREN, the customer's income is distributed to every child on average. For the same income, if this person has a large family and many children, his burden may be heavy and the possibility of default may be higher

-

HAS_HOUSE_INFORMATION: Here we design a binary feature according to whether the customer has missing house information. If it is not missing, it is 1 and the missing is 0

train["CREDIT_INCOME_PERCENT"]=(train["AMT_CREDIT"]/train["AMT_INCOME_TOTAL"]).round(2) train['ANNUITY_INCOME_PERCENT'] = (train['AMT_ANNUITY'] /train['AMT_INCOME_TOTAL']).round(2) train['CREDIT_TERM'] =(train['AMT_ANNUITY'] /train['AMT_CREDIT']).round(2) train['DAYS_EMPLOYED_PERCENT'] = (train['DAYS_EMPLOYED'] /train['DAYS_BIRTH']).round(2) train['INCOME_PER_CHILD'] = (train['AMT_INCOME_TOTAL'] /train['CNT_CHILDREN']).round(2) train['HAS_HOUSE_INFORMATION'] = train['COMMONAREA_MEDI'].apply(lambda x:1 if x>0 else 0)

Call the chart function defined above to observe the distribution of new features and default rate;

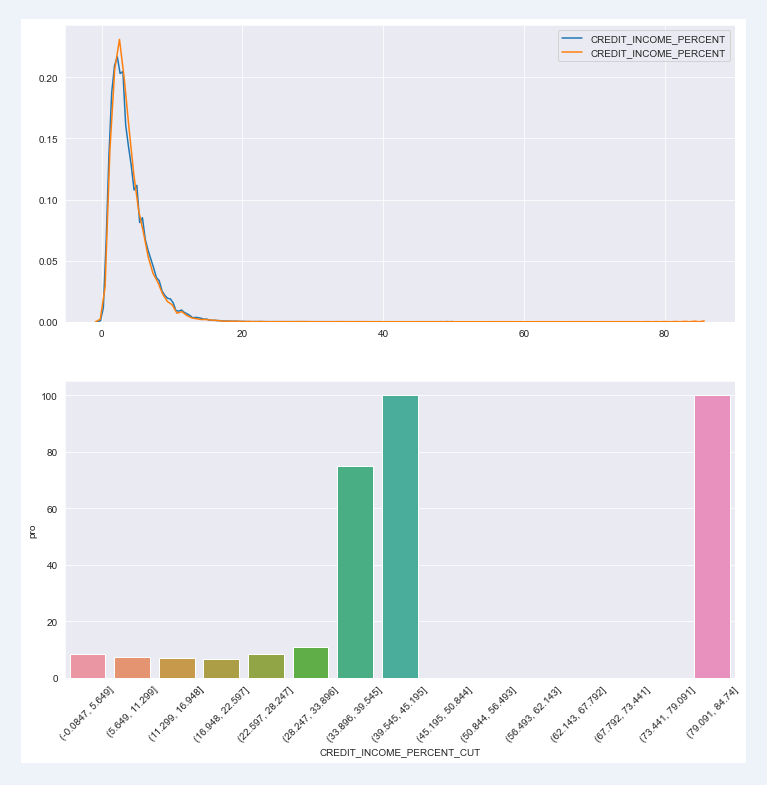

Loan amount / customer income: excluding extreme values and individual cases, the results shown in the distribution map are not quite consistent with our imagination; The question is whether to determine whether the features are invalid or remain and wait for the meeting to test the effect in the model, which is a question worthy of deep thinking and exploration

chart_fuc(train,"CREDIT_INCOME_PERCENT",con_ornot="continuity",cutn=15)

Default rate of each segment

CREDIT_INCOME_PERCENT_CUT sum count pro

0 (-0.0847, 5.649] 20083 242503 8.28

1 (5.649, 11.299] 4305 58657 7.34

2 (11.299, 16.948] 386 5685 6.79

3 (16.948, 22.597] 35 535 6.54

4 (22.597, 28.247] 8 96 8.33

5 (28.247, 33.896] 3 28 10.71

6 (33.896, 39.545] 3 4 75.00

7 (39.545, 45.195] 1 1 100.00

8 (45.195, 50.844] 0 1 0.00

9 (50.844, 56.493] 0 0 NaN

10 (56.493, 62.143] 0 0 NaN

11 (62.143, 67.792] 0 0 NaN

12 (67.792, 73.441] 0 0 NaN

13 (73.441, 79.091] 0 0 NaN

14 (79.091, 84.74] 1 1 100.00

Whether the applicant has housing information has a significant impact on the default rate. Moreover, users without real estate information account for the majority of the total user group. This is a problem. Whether the target group of the company itself has this feature or the point to be optimized needs to be discussed and analyzed in combination with the actual business

chart_fuc(train,"HAS_HOUSE_INFORMATION")

HAS_HOUSE_INFORMATION TARGET_SUM TARGET_COUNT Default_Rate 0 0 18998 223556 8.50 1 1 5827 83955 6.94

Modeling and prediction

If the model is LGB model, should the specific model be studied by Algorithm Engineers? There is a great God who can give directions to this part; If a person is proficient in the whole model process, including feature engineering and the underlying logic of the model, is he a "successful person"!!!

Differences and relations among lightgbm, xgboost and gbdt https://www.cnblogs.com/mata123/p/7440774.html

from sklearn.model_selection import KFold from sklearn.metrics import roc_auc_score from sklearn import preprocessing import lightgbm as lgb import gc

Modeling: model training

# The parameters are interpreted as training and test_data is the test set, encoding is the way to convert the classification field into value, one hot or LabelEncoder;

# Cross validation n_folds is the number of layers of training set (divided into training set and verification set)

def model(features, test_features, encoding = 'ohe', n_folds = 5):

# Extract the ID. the ID in the training set and test set has no effect on the feature and needs to be deleted

train_ids = features['SK_ID_CURR']

test_ids = test_features['SK_ID_CURR']

# Target of extracting training set: default 0 1;

labels = features['TARGET']

# Delete the target and ID in the training set to form a new training set (because the training set does not need the target and ID)

features = features.drop(columns = ['SK_ID_CURR', 'TARGET'])

test_features = test_features.drop(columns = ['SK_ID_CURR'])

# Convert the classification field to the attribute value field One Hot, corresponding to the LabelEncoder below

if encoding == 'ohe':

features = pd.get_dummies(features)

test_features = pd.get_dummies(test_features)

# Aligning the training set requires the field order of the test set, or the alignment feature order. inner indicates the alignment method. Delete the redundant columns (features) between the training set and the test set

features,test_features = features.align(test_features, join = 'inner', axis = 1)

# No categorical indications to record

cat_indices = 'auto'

# Assign labels to a 0-n_ Integers between classes-1, standardized. One Hot is horizontal and LabelEncoder is vertical;

elif encoding == 'le':

# Create LabelEncoder instance object

le = LabelEncoder()

# An index used to record classification features

cat_indices = []

# Traverse each column. enumerate means enumerating elements one by one. It returns the elements and their corresponding indexes

for i, col in enumerate(features):

if features[col].dtype == 'object':

# Convert the classification features of training set and test set into integers in the way of LabelEncoder

features[col] = le.fit_transform(np.array(features[col].astype(str)).reshape((-1,)))

test_features[col] = le.transform(np.array(test_features[col].astype(str)).reshape((-1,)))

# Record the classification index, and the results are [3, 4, 5, 11, 12, 13, 14, 15, 28, 32, 40, 86, 87, 89, 90]

cat_indices.append(i)

# One of the conversion methods of One Hot or LabelEncoder must be selected

else:

raise ValueError("Encoding must be either 'ohe' or 'le'")

print('Training Data Shape: ', features.shape)

print('Testing Data Shape: ', test_features.shape)

# Record feature name, i.e. column name

feature_names = list(features.columns)

# Convert DataFrame to tuple

features = np.array(features)

test_features = np.array(test_features)

# Create kfold instance object to form training set and verification set, n_folds is the parameter defined by the model function

k_fold = KFold(n_splits = n_folds, shuffle = True, random_state = 50)

# 0 tuple used to record feature importance

feature_importance_values = np.zeros(len(feature_names))

# 0 tuple used to record test set prediction results

test_predictions = np.zeros(test_features.shape[0])

# 0 tuple used to record the result of training set

out_of_fold = np.zeros(features.shape[0])

# Lists for recording validation and training scores

valid_scores = []

train_scores = []

# The training set is divided into new training set and verification set through kfold, and the training model is established

for train_indices, valid_indices in k_fold.split(features):

# Default label corresponding to the new training set

train_features, train_labels = features[train_indices], labels[train_indices]

# Validation set and default label corresponding to validation set

valid_features, valid_labels = features[valid_indices], labels[valid_indices]

# Instantiated LGB model

model = lgb.LGBMClassifier(n_estimators=1000, objective = 'binary',

class_weight = 'balanced', learning_rate = 0.05,

reg_alpha = 0.1, reg_lambda = 0.1,

subsample = 0.8, n_jobs = -1, random_state = 50)

# Training model

model.fit(train_features, train_labels, eval_metric = 'auc',

eval_set = [(valid_features, valid_labels), (train_features, train_labels)],

eval_names = ['valid', 'train'], categorical_feature = cat_indices,

early_stopping_rounds = 100, verbose = 200)

# Record the best iteration

best_iteration = model.best_iteration_

# Importance of recording characteristics

feature_importance_values += model.feature_importances_ / k_fold.n_splits

# Training set prediction

test_predictions += model.predict_proba(test_features, num_iteration = best_iteration)[:, 1] / k_fold.n_splits

# Record the prediction of the validation set

out_of_fold[valid_indices] = model.predict_proba(valid_features, num_iteration = best_iteration)[:, 1]

# Record high score

valid_score = model.best_score_['valid']['auc']

train_score = model.best_score_['train']['auc']

valid_scores.append(valid_score)

train_scores.append(train_score)

# Clear memory

gc.enable()

del model, train_features, valid_features

gc.collect()

# Record the prediction results of the training set, DataFrame structure

submission = pd.DataFrame({'SK_ID_CURR': test_ids, 'TARGET': test_predictions})

# Record feature importance, DataFrame structure

feature_importances = pd.DataFrame({'feature': feature_names, 'importance': feature_importance_values})

# Overall verification score: roc curve area

valid_auc = roc_auc_score(labels, out_of_fold)

# Verification set score and training set score

valid_scores.append(valid_auc)

train_scores.append(np.mean(train_scores))

# Record all validation sets and overall scores

fold_names = list(range(n_folds))

fold_names.append('overall')

# Record all validation sets and overall scores, DataFrame structure

metrics = pd.DataFrame({'fold': fold_names,

'train': train_scores,

'valid': valid_scores})

# Returns the prediction result, feature importance and model score of the training set

return submission, feature_importances, metrics

Model ROC score

submission, fi, metrics = model(train,test)

print("=="*50)

print("Model ROC score\n",metrics)

Training Data Shape: (307511, 241)

Testing Data Shape: (48744, 241)

Training until validation scores don't improve for 100 rounds

[200] train's auc: 0.7986 train's binary_logloss: 0.547763 valid's auc: 0.755506 valid's binary_logloss: 0.563315

[400] train's auc: 0.828273 train's binary_logloss: 0.518238 valid's auc: 0.755427 valid's binary_logloss: 0.545289

Early stopping, best iteration is:

[355] train's auc: 0.822307 train's binary_logloss: 0.524257 valid's auc: 0.755636 valid's binary_logloss: 0.548978

Training until validation scores don't improve for 100 rounds

[200] train's auc: 0.798864 train's binary_logloss: 0.547653 valid's auc: 0.758325 valid's binary_logloss: 0.563454

Early stopping, best iteration is:

[245] train's auc: 0.806436 train's binary_logloss: 0.540255 valid's auc: 0.758595 valid's binary_logloss: 0.558896

Training until validation scores don't improve for 100 rounds

[200] train's auc: 0.797785 train's binary_logloss: 0.549132 valid's auc: 0.76297 valid's binary_logloss: 0.56397

Early stopping, best iteration is:

[244] train's auc: 0.805083 train's binary_logloss: 0.542037 valid's auc: 0.763298 valid's binary_logloss: 0.559489

Training until validation scores don't improve for 100 rounds

[200] train's auc: 0.798991 train's binary_logloss: 0.547787 valid's auc: 0.758187 valid's binary_logloss: 0.562107

Early stopping, best iteration is:

[245] train's auc: 0.806411 train's binary_logloss: 0.540463 valid's auc: 0.758239 valid's binary_logloss: 0.557764

Training until validation scores don't improve for 100 rounds

[200] train's auc: 0.798045 train's binary_logloss: 0.548459 valid's auc: 0.757937 valid's binary_logloss: 0.564587

[400] train's auc: 0.828024 train's binary_logloss: 0.518946 valid's auc: 0.757796 valid's binary_logloss: 0.54673

Early stopping, best iteration is:

[315] train's auc: 0.816215 train's binary_logloss: 0.53072 valid's auc: 0.75831 valid's binary_logloss: 0.553896

====================================================================================================

Model ROC score

fold train valid

0 0 0.822307 0.755636

1 1 0.806436 0.758595

2 2 0.805083 0.763298

3 3 0.806411 0.758239

4 4 0.816215 0.758310

5 overall 0.811290 0.758783

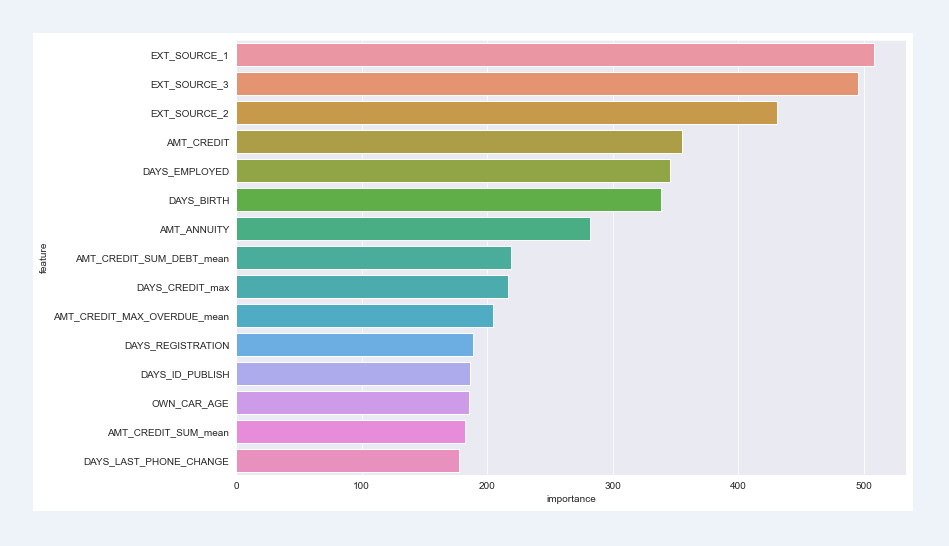

Feature importance top15

It can be seen that the impact of external data on default is more prominent. In other words, the prediction data given by the outside is more referential. In addition to external data, the user's age, working years, income, loan amount, car years, and population distribution in the customer's living area also have a great impact on the breach of contract

fi15=fi.sort_values("importance",ascending=False).head(15)

plt.figure(figsize=(12,8))

sns.set_style("darkgrid")

sns.barplot(x="importance",y="feature",data=fi15,orient="h")

<matplotlib.axes._subplots.AxesSubplot at 0x25887eb0>

There are also some features that have a weak impact on user breach of contract, such as the type of customer work organization and the situation of accompanying personnel during application, which may be inconsistent with our understanding in fact. It is also possible that the situation abroad is different from that at home. In short, it needs to be comprehensively analyzed in combination with the actual business products. The impact of a feature at the moment on default does not explain the future. Therefore, if you want to completely delete the data acquisition of a feature, you still need to make a careful decision;

fil15=fi.sort_values("importance",ascending=True).head(25)

fil15

| feature | importance | |

|---|---|---|

| 121 | NAME_INCOME_TYPE_Pensioner | 0.0 |

| 185 | ORGANIZATION_TYPE_Industry: type 13 | 0.0 |

| 190 | ORGANIZATION_TYPE_Industry: type 6 | 0.0 |

| 192 | ORGANIZATION_TYPE_Industry: type 8 | 0.0 |

| 173 | ORGANIZATION_TYPE_Cleaning | 0.0 |

| 199 | ORGANIZATION_TYPE_Mobile | 0.0 |

| 204 | ORGANIZATION_TYPE_Religion | 0.0 |

| 78 | FLAG_DOCUMENT_2 | 0.0 |

| 80 | FLAG_DOCUMENT_4 | 0.0 |

| 83 | FLAG_DOCUMENT_7 | 0.0 |

| 216 | ORGANIZATION_TYPE_Trade: type 5 | 0.0 |

| 86 | FLAG_DOCUMENT_10 | 0.0 |

| 88 | FLAG_DOCUMENT_12 | 0.0 |

| 96 | FLAG_DOCUMENT_20 | 0.0 |

| 224 | ORGANIZATION_TYPE_XNA | 0.0 |

| 105 | NAME_CONTRACT_TYPE_Revolving loans | 0.0 |

| 182 | ORGANIZATION_TYPE_Industry: type 10 | 0.0 |

| 14 | FLAG_CONT_MOBILE | 0.0 |

| 109 | FLAG_OWN_CAR_Y | 0.0 |

| 119 | NAME_INCOME_TYPE_Businessman | 0.0 |

| 12 | FLAG_EMP_PHONE | 0.0 |

| 11 | FLAG_MOBIL | 0.0 |

| 123 | NAME_INCOME_TYPE_Student | 0.0 |

| 114 | NAME_TYPE_SUITE_Group of people | 0.0 |

| 97 | FLAG_DOCUMENT_21 | 0.2 |

So far, even if a complete model prediction process is over, the total score of the model is within the acceptable range, which is a reference for users' review. The following is to extract new features from auxiliary set data to improve the model and improve the effect of the model.

Other dataset information

bureau=pd.read_csv(r"C:\Users\TP\Desktop\myself\Loan risk\Credit risk data set\bureau.csv")

Discrete variable (characterized by discrete type)

There are various ways to convert discrete variables into eigenvalues, which can be determined according to the model score in combination with the actual business or through the training model. For example, credit in bureau of credit information_ Active users may have multiple credit cards with different statuses, 'Closed', 'active', 'Sold', 'Bad debt'. Treatment method 1: we can only keep the state with the highest risk and delete others. For example, if the user has both 'active' and 'Bad debt', we can keep 'Bad debt' and delete 'active'; Processing method 2: we use the statistical function count to record the number of each state to form a new feature field; Although many companies adopt the first processing method, here we adopt the second one for convenience and define a unified discrete variable processing function;

#Definition of discrete variable processing function

def dispersed_featrue(data,featrue):

dg=data.groupby(["SK_ID_CURR",featrue])[featrue].count()

# Fill null values with 0

dc=dg.unstack(fill_value=0)

# New field naming

col=[]

for i in np.arange(len(dc.columns)):

new_col=featrue + "_" + dc.columns[i]

col.append(new_col)

dc.columns=col

dc.reset_index(inplace=True)

return dc

#There is another convenient method: get_dummies, no more details

Continuous variable (characterized by continuous type)

Continuous variables can be described by one or more of the mean, quantile, mode, variance, etc. in the statistical value

# Definition of continuous variable processing function

def continuos_featrue(data,featrue,statistics):

df=data.groupby("SK_ID_CURR")[featrue].agg(statistics)

df.reset_index(inplace=True)

# New field naming

col=["SK_ID_CURR"]

for i in np.arange(len(df.columns)-1):

new_col=featrue + "_" + df.columns[i+1]

col.append(new_col)

df.columns=col

return df

Convert the discrete variables and continuous variables in the credit report into analytical features with the above defined functions;

Discrete variable: CREDIT_ACTIVE (credit report status), CREDIT_CURRENCY, CREDIT_TYPE (loan type)

Continuous variable: DAYS_CREDIT (how many days before the current application, the customer has applied for credit)_ DAY_ Overdue (when the customer in the sample applies for a loan, how many days will the previously applied loan expire), AMT_ CREDIT_ MAX_ Overdrue (the highest amount of customer loan so far), CNT_CREDIT_PROLONG (times of deferred repayment in the customer's previous loan), AMT_CREDIT_SUM (loan limit of credit institution), AMT_CREDIT_SUM_DEBT (current debt of credit institutions), AMT_CREDIT_SUM_LIMIT (current credit card limit), AMT_CREDIT_SUM_ Overdrue (overdue amount of loans from credit institutions), AMT_ANNUITY (annual loan limit of credit institution)

# discrete variable ca=dispersed_featrue(bureau,"CREDIT_ACTIVE") cc=dispersed_featrue(bureau,"CREDIT_CURRENCY") ct=dispersed_featrue(bureau,"CREDIT_TYPE")

#continuous variable dc=continuos_featrue(bureau,"DAYS_CREDIT",["mean","max"]) cdo=continuos_featrue(bureau,"CREDIT_DAY_OVERDUE",["mean","max"]) acmo=continuos_featrue(bureau,"AMT_CREDIT_MAX_OVERDUE",["mean","max"]) ccp=continuos_featrue(bureau,"CNT_CREDIT_PROLONG",["mean","max"]) acs=continuos_featrue(bureau,"AMT_CREDIT_SUM",["mean","max","sum"]) acd=continuos_featrue(bureau,"AMT_CREDIT_SUM_DEBT",["mean","max","sum"]) acsl=continuos_featrue(bureau,"AMT_CREDIT_SUM_LIMIT",["mean","max","sum"]) acso=continuos_featrue(bureau,"AMT_CREDIT_SUM_OVERDUE",["mean","max","sum"]) aa=continuos_featrue(bureau,"AMT_ANNUITY",["mean","max","sum"])

Connect to the training set to form a new training set

col=[ca,cc,ct,dc,cdo,acmo,ccp,acs,acd,acsl,acso,aa]

for i in np.arange(len(col)):

train=pd.merge(train,col[i],how="inner",on="SK_ID_CURR")

test=pd.merge(test,col[i],how="inner",on="SK_ID_CURR")

train.head()

| SK_ID_CURR | TARGET | NAME_CONTRACT_TYPE | CODE_GENDER | FLAG_OWN_CAR | FLAG_OWN_REALTY | CNT_CHILDREN | AMT_INCOME_TOTAL | AMT_CREDIT | AMT_ANNUITY | ... | AMT_CREDIT_SUM_DEBT_sum | AMT_CREDIT_SUM_LIMIT_mean | AMT_CREDIT_SUM_LIMIT_max | AMT_CREDIT_SUM_LIMIT_sum | AMT_CREDIT_SUM_OVERDUE_mean | AMT_CREDIT_SUM_OVERDUE_max | AMT_CREDIT_SUM_OVERDUE_sum | AMT_ANNUITY_mean | AMT_ANNUITY_max | AMT_ANNUITY_sum | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 100002 | 1 | Cash loans | M | N | Y | 0 | 202500.0 | 406597.5 | 24700.5 | ... | 245781.0 | 7997.14125 | 31988.565 | 31988.565 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 1 | 100003 | 0 | Cash loans | F | N | N | 0 | 270000.0 | 1293502.5 | 35698.5 | ... | 0.0 | 202500.00000 | 810000.000 | 810000.000 | 0.0 | 0.0 | 0.0 | NaN | NaN | 0.0 |

| 2 | 100004 | 0 | Revolving loans | M | Y | Y | 0 | 67500.0 | 135000.0 | 6750.0 | ... | 0.0 | 0.00000 | 0.000 | 0.000 | 0.0 | 0.0 | 0.0 | NaN | NaN | 0.0 |

| 3 | 100007 | 0 | Cash loans | M | N | Y | 0 | 121500.0 | 513000.0 | 21865.5 | ... | 0.0 | 0.00000 | 0.000 | 0.000 | 0.0 | 0.0 | 0.0 | NaN | NaN | 0.0 |

| 4 | 100008 | 0 | Cash loans | M | N | Y | 0 | 99000.0 | 490495.5 | 27517.5 | ... | 240057.0 | 0.00000 | 0.000 | 0.000 | 0.0 | 0.0 | 0.0 | NaN | NaN | 0.0 |

5 rows × 174 columns

So far, a new training set has been formed combined with auxiliary data; According to the actual situation, there will be more new features. The data determines the upper limit of the model, and feature construction requires considerable business understanding, which is a fine activity. Feature construction is not explored here

As for the selection of features, some features with collinearity are excluded to improve the effect of the model. The correlation coefficient between variables can be calculated to quickly remove some variables with high correlation. Here, a threshold value of 0.8 can be defined, that is, remove one of the variables in each pair of variables with correlation greater than 0.8;

In addition, variables insensitive to the target response will also affect the accuracy of the model. These variables can be deleted according to the correlation coefficient or the importance of model characteristics. The reason is the same as above and will not be repeated;

df=train.drop(columns=["SK_ID_CURR","TARGET"])

df=df.corr()

# Define an empty list to record the features that need to be deleted because the correlation is greater than 0.8

ft=[]

for col in df:

if col not in ft:

d=df.index[df[col] >0.8].to_list()

if col in d :

d.remove(col)

ft.extend(d)

# Delete variables whose correlation is greater than the threshold

train.drop(columns=ft,inplace=True)

train.head()

| SK_ID_CURR | TARGET | NAME_CONTRACT_TYPE | CODE_GENDER | FLAG_OWN_CAR | FLAG_OWN_REALTY | CNT_CHILDREN | AMT_INCOME_TOTAL | AMT_CREDIT | AMT_ANNUITY | ... | AMT_CREDIT_SUM_mean | AMT_CREDIT_SUM_sum | AMT_CREDIT_SUM_DEBT_mean | AMT_CREDIT_SUM_DEBT_max | AMT_CREDIT_SUM_LIMIT_mean | AMT_CREDIT_SUM_LIMIT_max | AMT_CREDIT_SUM_OVERDUE_mean | AMT_CREDIT_SUM_OVERDUE_max | AMT_ANNUITY_mean | AMT_ANNUITY_max | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 100002 | 1 | Cash loans | M | N | Y | 0 | 202500.0 | 406597.5 | 24700.5 | ... | 108131.945625 | 865055.565 | 49156.2 | 245781.0 | 7997.14125 | 31988.565 | 0.0 | 0.0 | 0.0 | 0.0 |

| 1 | 100003 | 0 | Cash loans | F | N | N | 0 | 270000.0 | 1293502.5 | 35698.5 | ... | 254350.125000 | 1017400.500 | 0.0 | 0.0 | 202500.00000 | 810000.000 | 0.0 | 0.0 | NaN | NaN |

| 2 | 100004 | 0 | Revolving loans | M | Y | Y | 0 | 67500.0 | 135000.0 | 6750.0 | ... | 94518.900000 | 189037.800 | 0.0 | 0.0 | 0.00000 | 0.000 | 0.0 | 0.0 | NaN | NaN |

| 3 | 100007 | 0 | Cash loans | M | N | Y | 0 | 121500.0 | 513000.0 | 21865.5 | ... | 146250.000000 | 146250.000 | 0.0 | 0.0 | 0.00000 | 0.000 | 0.0 | 0.0 | NaN | NaN |

| 4 | 100008 | 0 | Cash loans | M | N | Y | 0 | 99000.0 | 490495.5 | 27517.5 | ... | 156148.500000 | 468445.500 | 80019.0 | 240057.0 | 0.00000 | 0.000 | 0.0 | 0.0 | NaN | NaN |

5 rows × 126 columns

Retraining model

submission, fi, metrics = model(train,test)

print("=="*50)

print("Model ROC score\n",metrics)

Training Data Shape: (263491, 239)

Testing Data Shape: (42320, 239)

Training until validation scores don't improve for 100 rounds

[200] train's auc: 0.814678 train's binary_logloss: 0.532306 valid's auc: 0.766264 valid's binary_logloss: 0.5511

Early stopping, best iteration is:

[249] train's auc: 0.823937 train's binary_logloss: 0.522804 valid's auc: 0.766576 valid's binary_logloss: 0.545026

Training until validation scores don't improve for 100 rounds

[200] train's auc: 0.814559 train's binary_logloss: 0.532478 valid's auc: 0.767164 valid's binary_logloss: 0.551391

Early stopping, best iteration is:

[283] train's auc: 0.830264 train's binary_logloss: 0.516345 valid's auc: 0.767488 valid's binary_logloss: 0.541334

Training until validation scores don't improve for 100 rounds

[200] train's auc: 0.814355 train's binary_logloss: 0.533096 valid's auc: 0.771143 valid's binary_logloss: 0.549807

Early stopping, best iteration is:

[284] train's auc: 0.830247 train's binary_logloss: 0.516858 valid's auc: 0.771516 valid's binary_logloss: 0.539648

Training until validation scores don't improve for 100 rounds

[200] train's auc: 0.815806 train's binary_logloss: 0.530951 valid's auc: 0.75585 valid's binary_logloss: 0.550364

Early stopping, best iteration is:

[297] train's auc: 0.833183 train's binary_logloss: 0.512621 valid's auc: 0.756601 valid's binary_logloss: 0.538989

Training until validation scores don't improve for 100 rounds

[200] train's auc: 0.813839 train's binary_logloss: 0.532965 valid's auc: 0.767956 valid's binary_logloss: 0.548167

Early stopping, best iteration is:

[210] train's auc: 0.81593 train's binary_logloss: 0.530808 valid's auc: 0.768212 valid's binary_logloss: 0.546807

====================================================================================================

Model ROC score

fold train valid

0 0 0.823937 0.766576

1 1 0.830264 0.767488

2 2 0.830247 0.771516

3 3 0.833183 0.756601

4 4 0.815930 0.768212

5 overall 0.826712 0.765973

fi15=fi.sort_values("importance",ascending=False).head(15)

plt.figure(figsize=(12,8))

sns.set_style("darkgrid")

sns.barplot(x="importance",y="feature",data=fi15,orient="h")

<matplotlib.axes._subplots.AxesSubplot at 0x2b2f4790>

Adding a new training set composed of new features filtered by the auxiliary training set to train the model, the result is better than the original training set training model. It can also be seen from the feature importance that some features constructed through the auxiliary training set are also of high importance and perform well

So far, the whole model building process has ended; Model building is a continuous iterative process, including feature engineering optimization, new data collection, algorithm optimization and so on.