catalogue

2.1 random forest classifier function and its parameters

2.2 construction of random forest

2.3 comparison of random forest and decision tree under cross validation

2.4 drawing n_ Learning curve of estimators

3.1 random forest classifier function and its parameters

3.2 filling missing values with random forest regression

4 basic idea of machine learning parameter adjustment

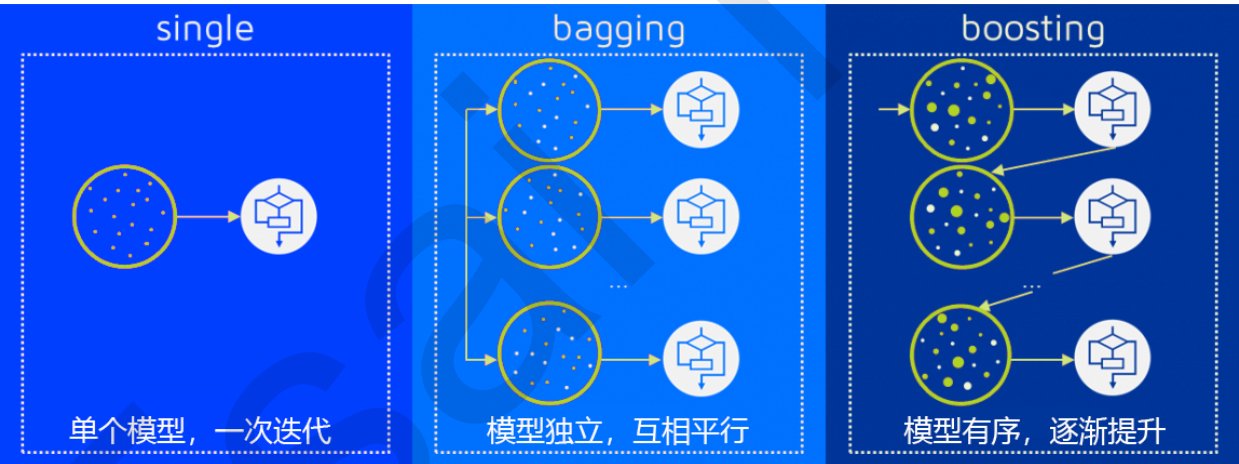

1 integrated learning

Ensemble learning completes the learning task by building and combining multiple learners. It is not a single machine learning algorithm, but by building multiple models on the data to integrate the modeling results of all models. It can be used to model marketing simulation, count customer sources, retention and loss, and predict the risk of disease and the susceptibility of patients.

The integration algorithm will consider the modeling results of multiple evaluators and summarize them to obtain a comprehensive result, so as to obtain better regression or classification performance than a single model.

The model integrated by multiple models is called an integrated estimator, and each model constituting the integrated estimator is called a base estimator. Generally speaking, there are three kinds of integration algorithms: Bagging, Boosting and stacking.

To achieve good integration, individual learners should be "good but different", that is, individual learners should not only have certain accuracy, but also have differences between learners.

2 random forest classifier

2.1 random forest classifier function and its parameters

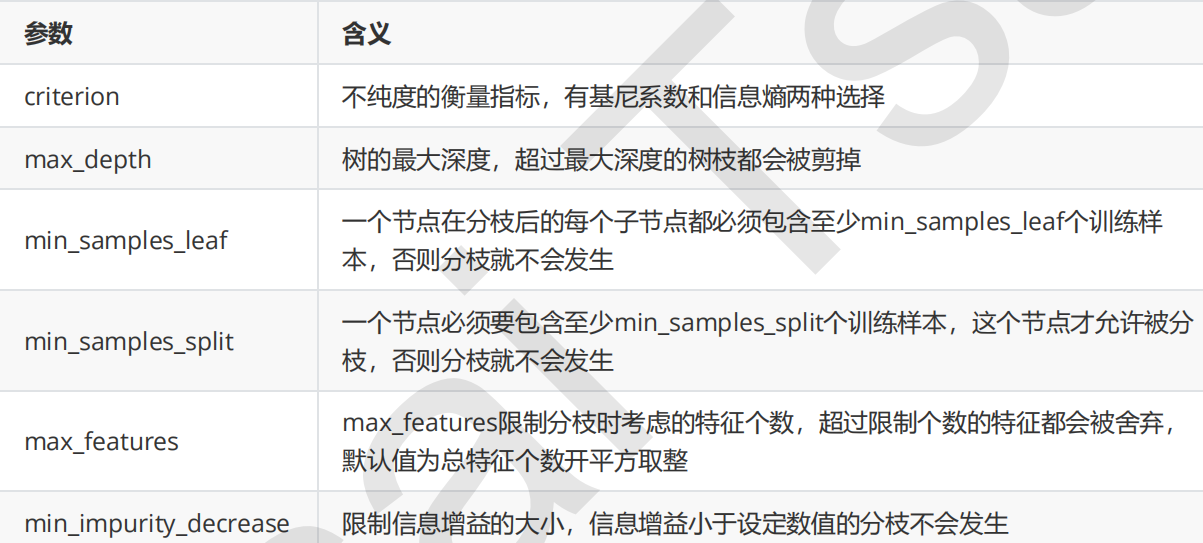

Many parameters of random forest classifier are consistent with those of decision tree. The parameters of the control base evaluator are as follows.

Other relevant parameters:

2.2 construction of random forest

On the red wine dataset, the effect of random forest is better than that of decision tree.

from sklearn.ensemble import RandomForestClassifier

from sklearn.tree import DecisionTreeClassifier

from sklearn.model_selection import train_test_split

from sklearn.datasets import load_wine

wine=load_wine()

Xtrain,Xtest,Ytrain,Ytest=train_test_split(wine.data,wine.target,test_size=0.3)

#instantiation

clf=DecisionTreeClassifier()

rfc=RandomForestClassifier()

clf=clf.fit(Xtrain,Ytrain)

rfc.fit(Xtrain,Ytrain)

score_c=clf.score(Xtest,Ytest)

score_r=rfc.score(Xtest,Ytest)

print("Single Tree:{}".format(score_c))

print("Random Forest:{}".format(score_r))

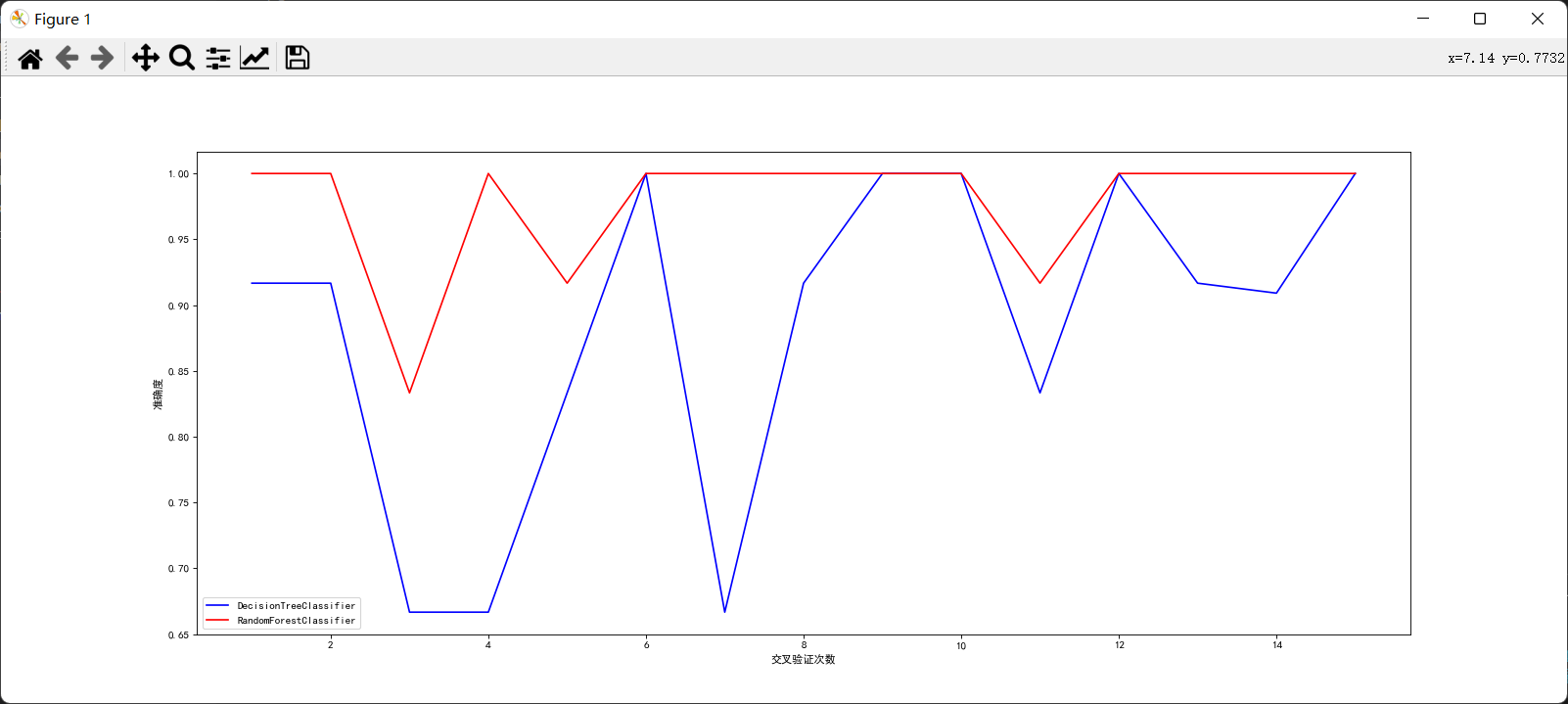

2.3 comparison of random forest and decision tree under cross validation

Through comparison, it can be found that the effect of random forest is indeed better than decision tree. Only in a few cases, the accuracy of the two is the same. At other times, random forest is better than decision tree.

from matplotlib import colors

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from sklearn.ensemble import RandomForestClassifier

from sklearn.tree import DecisionTreeClassifier

from sklearn.model_selection import train_test_split

from sklearn.model_selection import cross_val_score

from sklearn.datasets import load_wine

plt.rcParams['font.sans-serif']=['SimHei'] #Used to display Chinese labels normally

plt.rcParams['axes.unicode_minus']=False #Used to display negative signs normally

wine=load_wine()

Xtrain,Xtest,Ytrain,Ytest=train_test_split(wine.data,wine.target,test_size=0.3)

#instantiation

rfc=RandomForestClassifier(n_estimators=20) #Set number of base evaluators

clf=DecisionTreeClassifier()

#Perform cross validation

rfc_s=cross_val_score(rfc,wine.data,wine.target,cv=15)

clf_s=cross_val_score(clf,wine.data,wine.target,cv=15)

#mapping

plt.figure(figsize=(20,8),dpi=80)

plt.plot(range(1,16),clf_s,color='blue',label="DecisionTreeClassifier")

plt.plot(range(1,16),rfc_s,color='red',label="RandomForestClassifier")

plt.xlabel('Number of cross validation')

plt.ylabel('Accuracy')

plt.legend(loc='best')

plt.show()

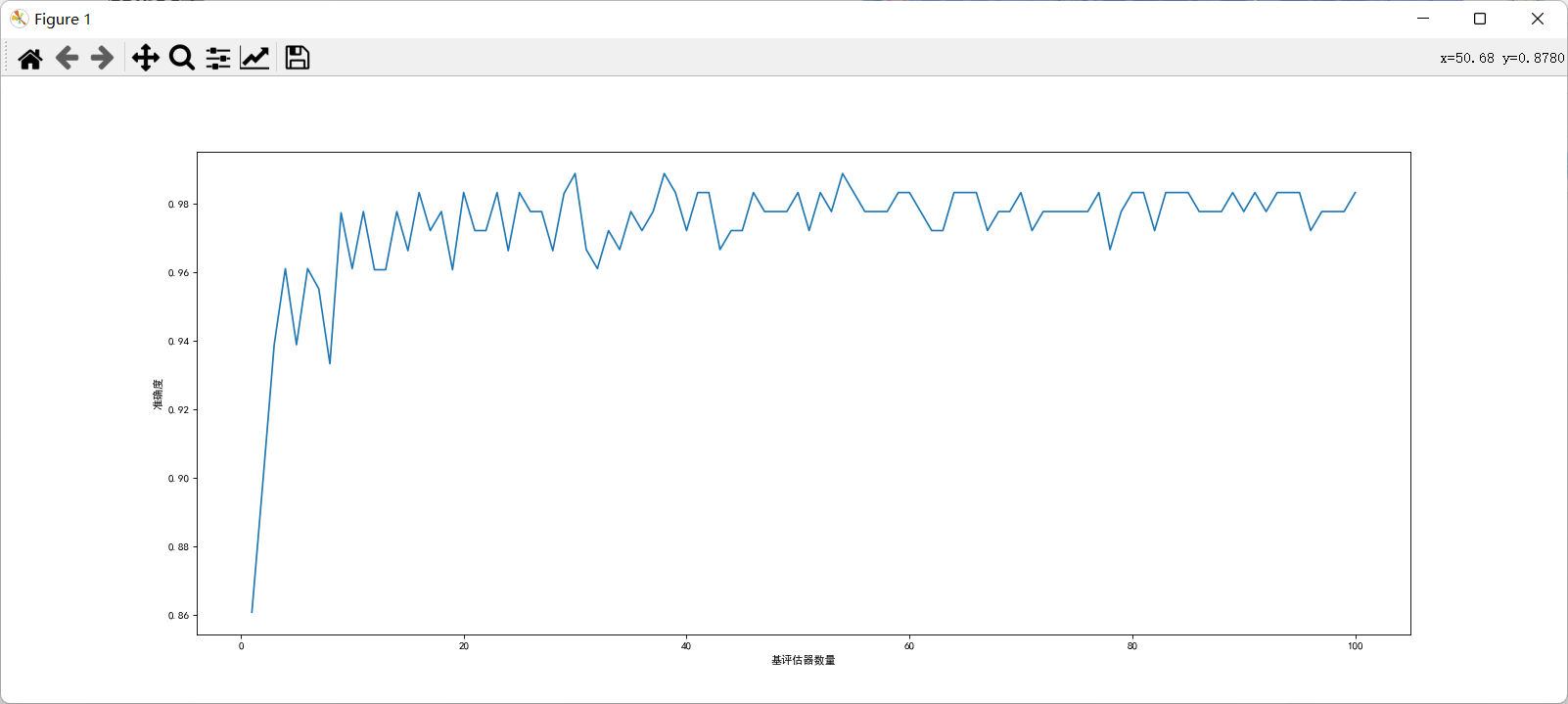

2.4 drawing n_ Learning curve of estimators

from matplotlib import colors

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from sklearn.ensemble import RandomForestClassifier

from sklearn.tree import DecisionTreeClassifier

from sklearn.model_selection import train_test_split

from sklearn.model_selection import cross_val_score

from sklearn.datasets import load_wine

plt.rcParams['font.sans-serif']=['SimHei'] #Used to display Chinese labels normally

plt.rcParams['axes.unicode_minus']=False #Used to display negative signs normally

wine=load_wine()

Xtrain,Xtest,Ytrain,Ytest=train_test_split(wine.data,wine.target,test_size=0.3)

score=[]

for i in range(100):

rfc=RandomForestClassifier(n_estimators=i+1)

rfc_s=cross_val_score(rfc,wine.data,wine.target,cv=10).mean()

score.append(rfc_s)

print("Highest accuracy{} Corresponding times{}".format(max(score),score.index(max(score))))

plt.figure(figsize=(20,8),dpi=80)

plt.plot(range(1,101),score)

plt.xlabel('Number of base evaluators')

plt.ylabel('Accuracy')

plt.show()

3 random forest regressor

3.1 random forest classifier function and its parameters

criterion:

3.2 filling missing values with random forest regression

For a data with n features, where feature t has missing values, we take feature t as a label, and the other n-1 features and the original label form a new feature matrix. For T, there is no missing part, that is, our Y_test, this part of the data has both labels and features, and the missing part has only features and no labels, which is the part we need to predict.

Other n-1 features corresponding to the value of feature T not missing + original label: X_train

Value of characteristic T not missing: Y_train

Other n-1 features corresponding to the missing value of feature T + original label: X_test

Missing value of characteristic T: unknown, we need to predict Y_test

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from pandas.core.frame import DataFrame

from sklearn.datasets import load_boston

from sklearn.impute import SimpleImputer

from sklearn.ensemble import RandomForestRegressor

from sklearn.model_selection import cross_val_score

boston=load_boston()

# print(boston)

# print(boston.data.shape)

#After storing the complete data set, the missing data set will be processed and filled, and then compared with the original data set

x_full,y_full=boston.data,boston.target #Storing original data and characteristics

n_samples=x_full.shape[0]#Record the number of complete samples

n_features=x_full.shape[1]#Record the number of complete features

#Put missing values for full data

#Determine the proportion of missing values, here we assume 50%

rng=np.random.RandomState(0)#Determine a random pattern

missing_rate=0.5

n_missing_samples=int(np.floor(n_samples*n_features*missing_rate))#Round down, resulting in the total number of missing data

# print(n_missing_samples)

#The generated missing values are distributed in each row and column of the data

miss_features=rng.randint(0,n_features,n_missing_samples) #The three parameters are the number of lower and upper limits in turn

miss_samples=rng.randint(0,n_samples,n_missing_samples)

#If the random number taken out is less than the sample size, the choice method can be used

#missing_samples = rng.choice(n_samples,n_missing_samples,replace=False) #The number of random fetches required when the parameters from left to right are the maximum will not be repeated to ensure more scattered data

#Create missing data

#Operate after copying the original complete data

x_missing=x_full.copy()

y_missing=y_full.copy()

#Replace a part of the complete data with a missing value

x_missing[miss_samples,miss_features]=np.nan

#Convert to dataframe to facilitate subsequent operations

x_missing=DataFrame(x_missing)

# print(x_missing)

#Filling missing values with mean

imp_mean=SimpleImputer(missing_values=np.nan,strategy='mean')#instantiation

x_missing_mean = imp_mean.fit_transform(x_missing) #fit_transform training + export predict

#Check whether the filling is completed

# print(pd.DataFrame(x_missing_mean).isnull().sum())

#Fill missing values with median

imp_median=SimpleImputer(missing_values=np.nan,strategy='median')#instantiation

x_missing_median = imp_median.fit_transform(x_missing) #fit_transform training + export predict

#Check whether the filling is completed

# print(pd.DataFrame(x_missing_median).isnull().sum())

#Fill with 0

imp_0 = SimpleImputer(missing_values=np.nan, strategy="constant",fill_value=0)

x_missing_0 = imp_0.fit_transform(x_missing)

#Check whether the filling is completed

# print(pd.DataFrame(x_missing_0).isnull().sum())

#Filling missing values with random forests

x_missing_reg=x_missing.copy()#Replicate matrices that require regression to fill in missing values

#The essence of finding out the order of the corresponding eigenvalues from small to large is to find the index and fill it from the one with the most missing values

sortindex=np.argsort(x_missing_reg.isnull().sum(axis=0)).values #argsort returns the index and uses values to fetch the data

#Traversal fill missing values

for i in sortindex:

#Build a new feature matrix (features not selected to be filled + original labels) and a new label (features selected to be filled)

df=x_missing_reg

fillc=df.iloc[:,i]

#New characteristic matrix

df=pd.concat([df.iloc[:,df.columns!=i],pd.DataFrame(y_full)],axis=1) #Left right connection

#In the new characteristic matrix, the columns with missing values are filled with 0

df_0 =SimpleImputer(missing_values=np.nan,strategy='constant',fill_value=0).fit_transform(df)

#Find training set and test set

Ytrain = fillc[fillc.notnull()] #Non empty in features selected to fill

Ytest = fillc[fillc.isnull()] #For those values that do not exist in the selected features to be filled, we need not the value of ytest, but its index

Xtrain = df_0[Ytrain.index,:] #On the new characteristic matrix, the record corresponding to the selected non null value

Xtest = df_0[Ytest.index,:] #On the new feature matrix, the record corresponding to the selected feature null value

#Filling missing values using random forests

rfc = RandomForestRegressor(n_estimators=100)

rfc = rfc.fit(Xtrain, Ytrain)

Ypredict = rfc.predict(Xtest)#Get the prediction results

#Fill the filled features into the original feature matrix

x_missing_reg.loc[x_missing_reg.iloc[:,i].isnull(),i]=Ypredict #First, use iloc to find the row index of nan

# print(x_missing_reg.isnull().sum())

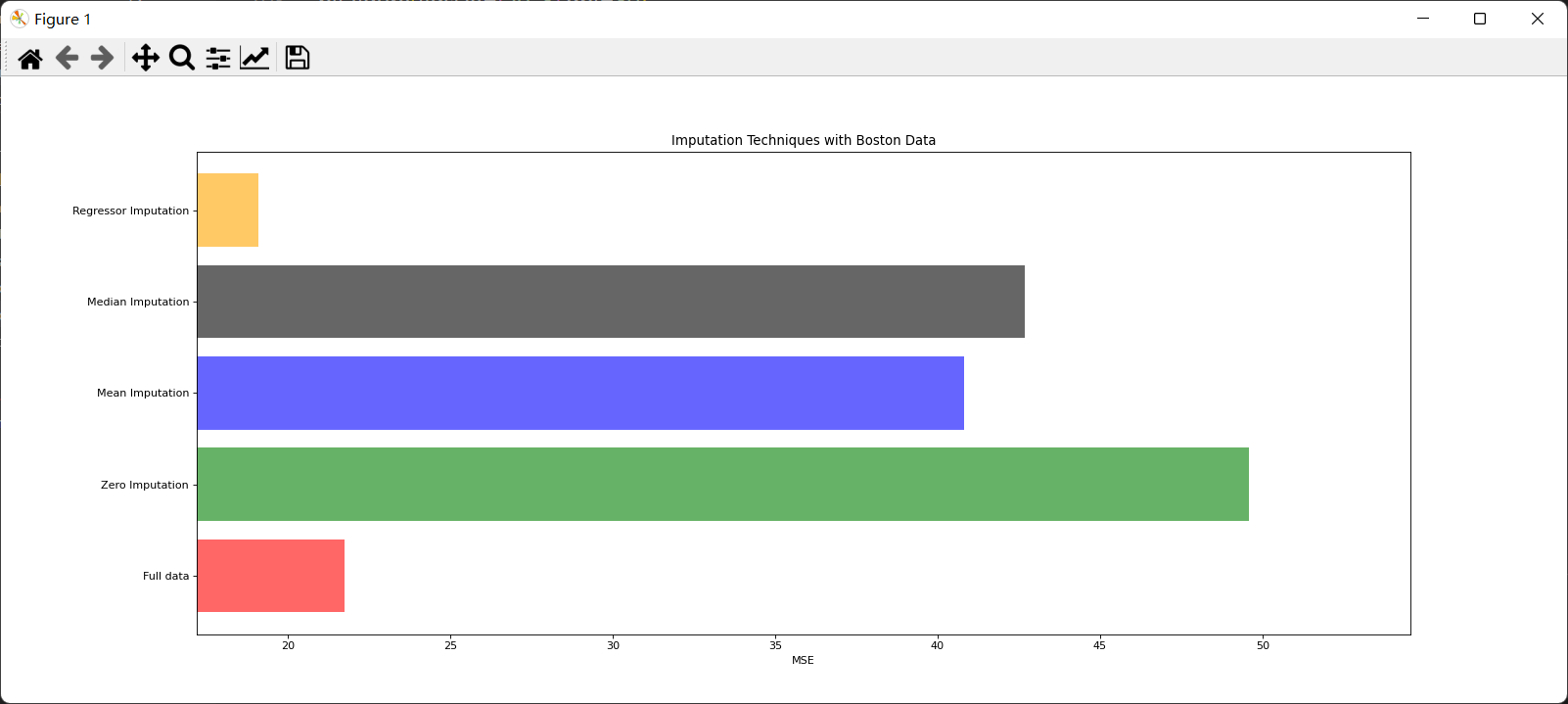

#All data were modeled and MSE results were obtained

X = [x_full,x_missing_0,x_missing_mean,x_missing_median,x_missing_reg]

mse = []

std = []

for x in X:

estimator = RandomForestRegressor()

scores = cross_val_score(estimator,x,y_full,scoring='neg_mean_squared_error', cv=5).mean()#Score with negative mean square error

mse.append(scores * -1)#Turn the result to positive

print(*zip(['x_full','x_missing_0','x_missing_mean','x_missing_median','x_missing_reg'],mse))#The smaller the better

#mapping

x_labels = ['Full data','Zero Imputation','Mean Imputation','Median Imputation','Regressor Imputation']

colors = ['r', 'g', 'b','black', 'orange']

plt.figure(figsize=(20, 8),dpi=80)

ax = plt.subplot(111) #Add subgraphs to prepare for subsequent functionalization

for i in np.arange(len(mse)):

ax.barh(i, mse[i],color=colors[i], alpha=0.6, align='center') #Draw the bar chart horizontally in the center

ax.set_title('Imputation Techniques with Boston Data')

ax.set_xlim(left=np.min(mse) * 0.9,right=np.max(mse) * 1.1)#The x-axis of the limited range is mse value

ax.set_yticks(np.arange(len(mse)))#Set y scale

ax.set_xlabel('MSE')

ax.set_yticklabels(x_labels)#Change y's scale

plt.show()4 basic idea of machine learning parameter adjustment

4.1 related concepts

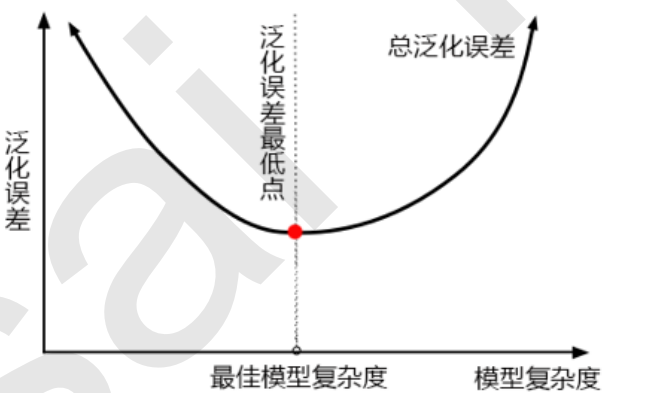

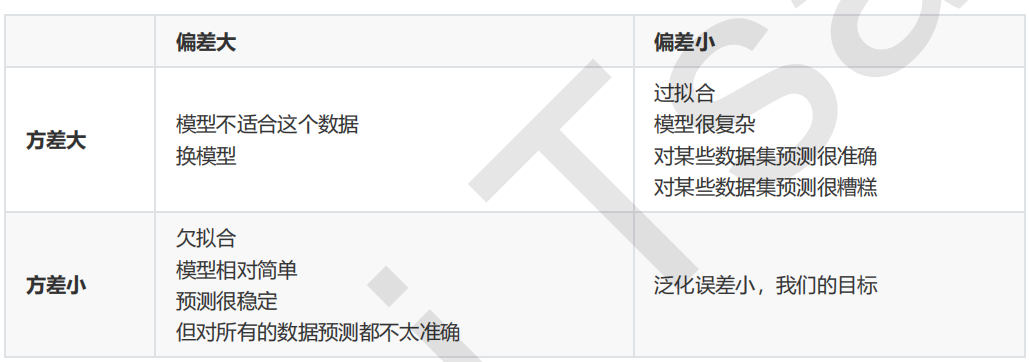

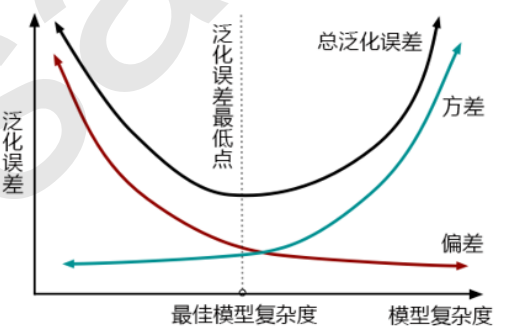

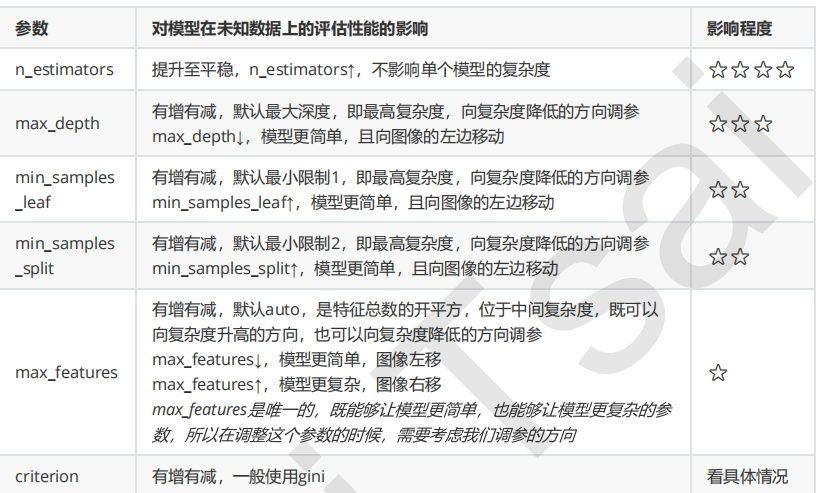

The first step in model tuning is to find the right goal: what are we going to do? Generally speaking, this goal is to improve the evaluation index of a model. For example, for random forests, what we want to improve is the accuracy of the model on unknown data (measured by score or oob_score_). To find this goal, we need to think: what factors affect the accuracy of the model on unknown data? In machine learning, the index we use to measure the accuracy of the model on unknown data is called generalization error.

4.2 examples

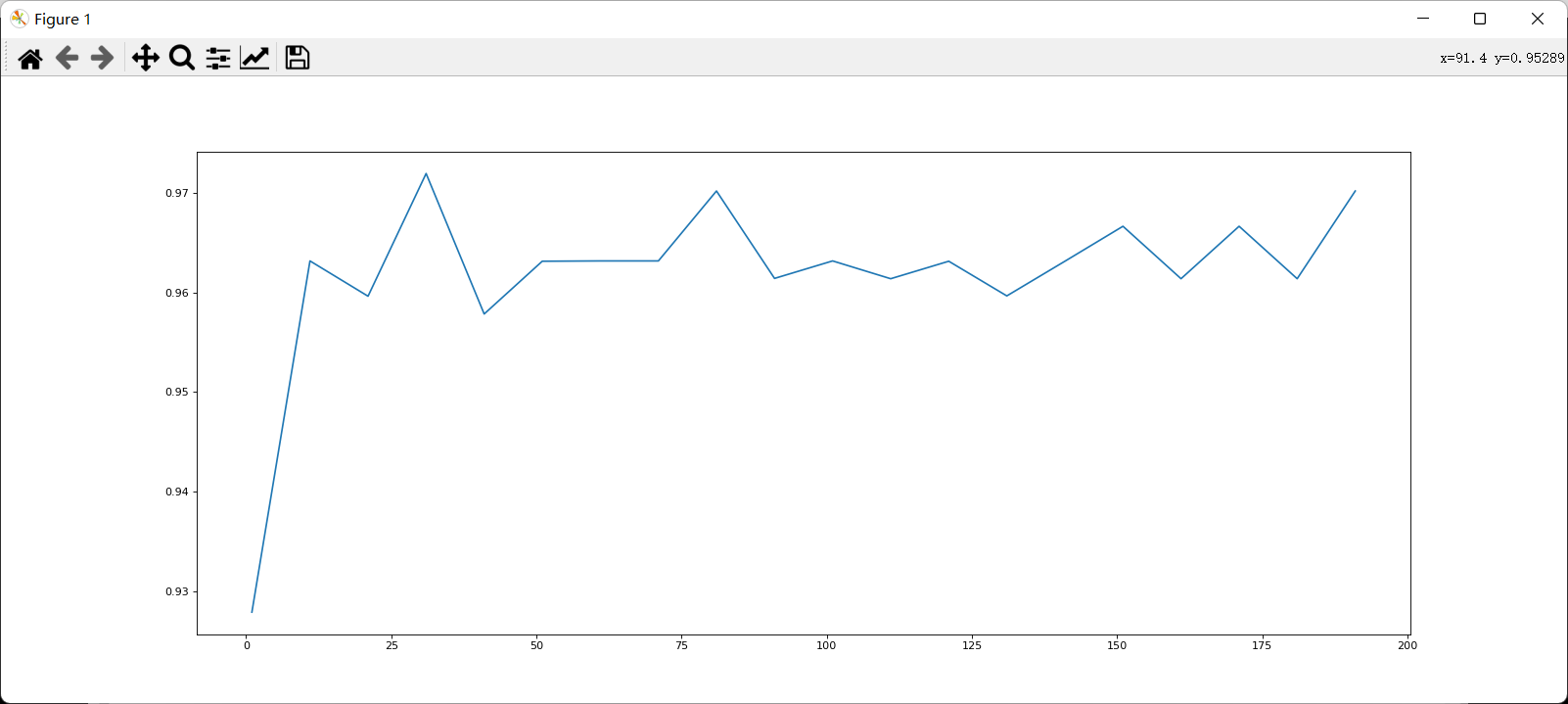

View n_ The learning curve of estimators.

After determining the good range, further refine the learning curve.

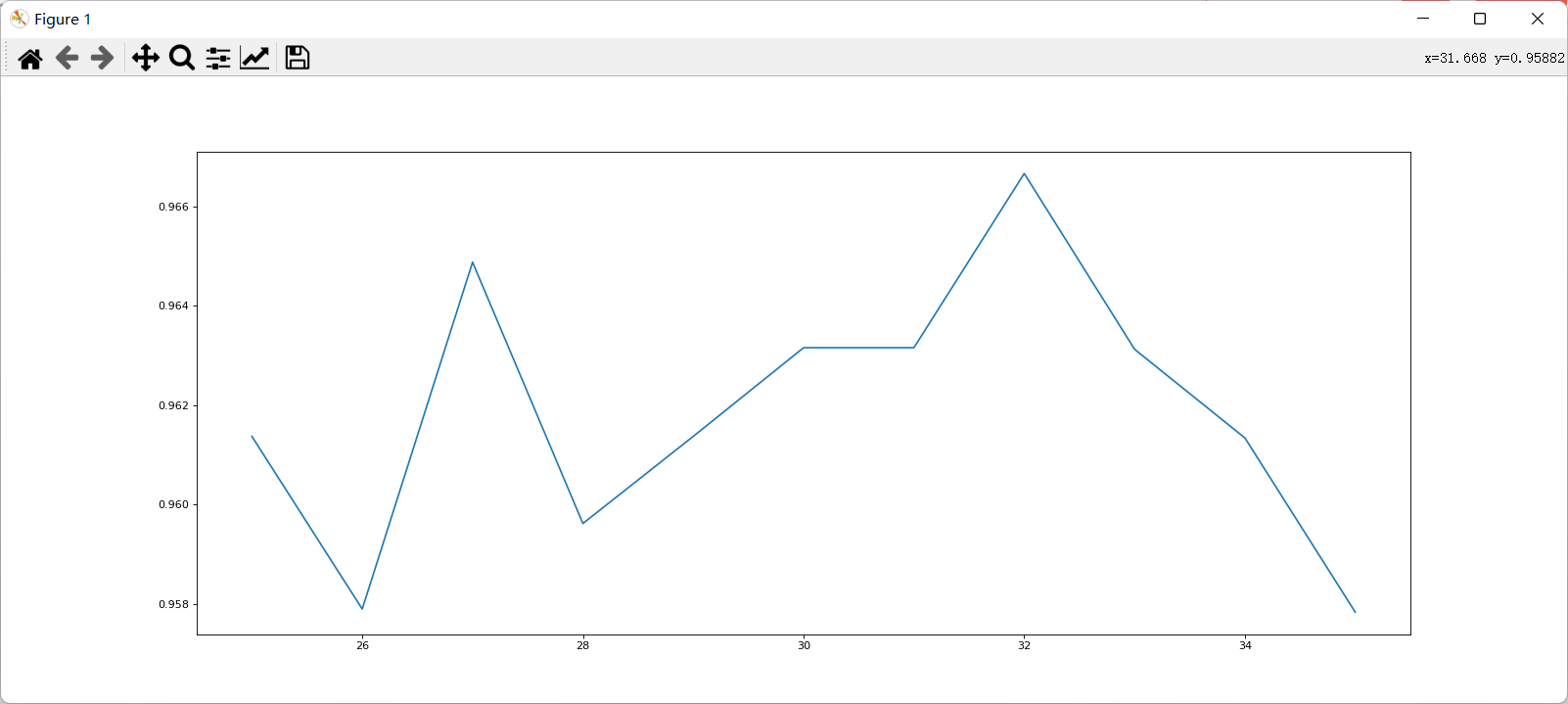

Because the division of each training set and test set is different, the performance after refinement may be worse than before, but in general, the refined curve can provide a more accurate parameter selection range. After determining the number of base evaluators, further use grid search to find other appropriate parameters.

Max is modulated_ After depth, the accuracy of the model increases, so the model is on the right side of the generalization complexity.

Min at this time_ samples_ Split reduces the accuracy, so the parameter is not set.

Adjust random_state

The accuracy is improved.

The complete code is as follows

from sklearn.datasets import load_breast_cancer

from sklearn.ensemble import RandomForestClassifier

from sklearn.model_selection import GridSearchCV

from sklearn.model_selection import cross_val_score

import matplotlib.pyplot as plt

import pandas as pd

import numpy as np

data = load_breast_cancer()

#preliminary estimates

# scorel = []

# for i in range(0,200,10):

# rfc=RandomForestClassifier(n_estimators=i+1)

# score=cross_val_score(rfc,data.data,data.target,cv=10).mean()

# scorel.append(score)

# print(max(scorel),(scorel.index(max(scorel))*10)+1)

# plt.figure(figsize=[20,8],dpi=80)

# plt.plot(range(1,201,10),scorel)

# plt.show()

#Refined estimation

# scorel = []

# for i in range(25,36):

# rfc=RandomForestClassifier(n_estimators=i+1)

# score=cross_val_score(rfc,data.data,data.target,cv=10).mean()

# scorel.append(score)

# print(max(scorel),([*range(25,36)][scorel.index(max(scorel))])) #Take the index corresponding to the maximum value in the range of 30-39

# plt.figure(figsize=[20,8],dpi=80)

# plt.plot(range(25,36),scorel)

# plt.show()

#Adjust max_depth

# param_grid = {'max_depth':np.arange(1, 20, 1)}

# Generally based on the size of the data to carry out a test, breast cancer data is very small, so you can use 1~10, or 1~20 test.

# However, for large data like digital recognition, we should try 30 ~ 50 layers of depth (maybe not enough)

# We should draw a learning curve to observe the influence of depth on the model

# rfc = RandomForestClassifier(n_estimators=32)

# GS = GridSearchCV(rfc,param_grid,cv=10)

# GS.fit(data.data,data.target)

# print(GS.best_params_,GS.best_score_)

#Adjust max_features

#Now that the model is on the right side of the image, we need lower complexity

#max_ The default minimum value of features is sqrt(n_features), so we use twice this value as the maximum value of the tuning range.

# param_grid = {'max_features':np.arange(1,10,1)}

# rfc = RandomForestClassifier(n_estimators=32,max_depth=11)

# GS = GridSearchCV(rfc,param_grid,cv=10)

# GS.fit(data.data,data.target)

# print(GS.best_params_,GS.best_score_)

#Adjustment min_samples_leaf

#For min_samples_split and min_samples_leaf is generally increased by 10 or 20 from their minimum value

#In the face of high-dimensional and high sample size data, if you are not confident, you can also directly + 50. For large data, you may need a range of 200 ~ 300

#If you find that the accuracy can not be improved in any case during adjustment, you can rest assured and boldly adjust a large data to greatly limit the complexity of the model

# param_grid={'min_samples_leaf':np.arange(1, 1+10, 1)}

# rfc = RandomForestClassifier(n_estimators=32,max_depth=11,max_features=7)

# GS = GridSearchCV(rfc,param_grid,cv=10)

# GS.fit(data.data,data.target)

# print(GS.best_params_,GS.best_score_)

#Adjust random_state

# param_grid={'random_state':np.arange(20,150)}

# rfc = RandomForestClassifier(n_estimators=32,max_depth=11,max_features=7)

# GS = GridSearchCV(rfc,param_grid,cv=10)

# GS.fit(data.data,data.target)

# print(GS.best_params_,GS.best_score_)

#Determine final parameters

rfc = RandomForestClassifier(n_estimators=39,max_depth=11,max_features=7,random_state=66)

score = cross_val_score(rfc,data.data,data.target,cv=10)

print(score)